Ask a fund manager why a stock outperformed and you’ll usually get a story — a great product, strong management, a market tailwind. Factor investing asks a different question: strip away the stories, and are there measurable, repeatable characteristics that have historically predicted which stocks outperform? Decades of academic research say yes, and Indian markets have generated enough data now to test these ideas locally rather than just importing conclusions from US equity research. Here’s what the three most persistent factors actually are, how they’ve behaved in India specifically, and how you can practically use this framework.

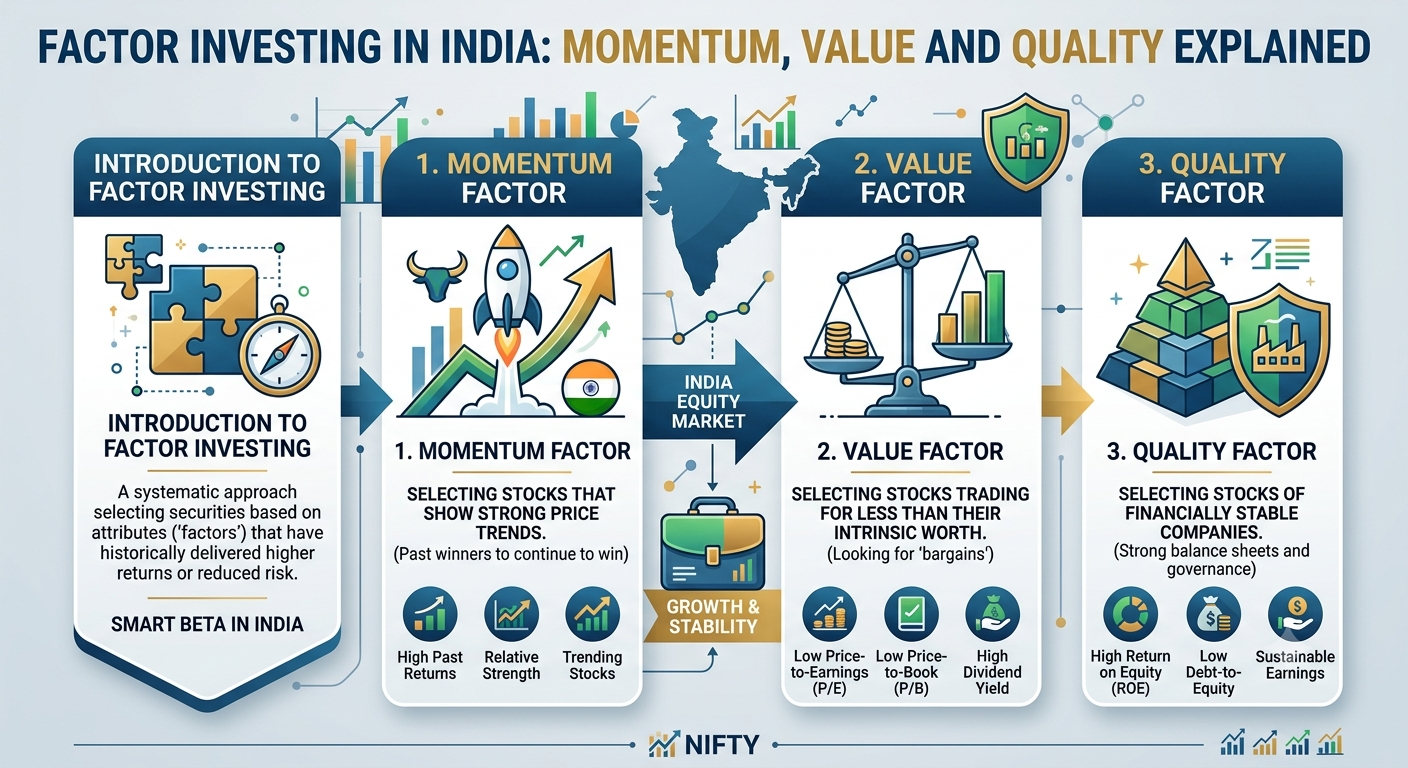

What a “factor” actually means

A factor is a measurable, quantifiable characteristic of a stock — not a story, a number. Momentum is quantified as trailing price performance over a defined lookback period. Value is quantified through ratios like price-to-earnings, price-to-book, or EV/EBITDA relative to peers or history. Quality is quantified through metrics like return on equity, earnings stability, and low debt. The core premise of factor investing is that stocks ranking favorably on these dimensions have, historically and across markets, delivered better risk-adjusted returns than the broad market over long horizons — not every year, but persistently enough to be more than noise.

Momentum: buying strength, not cheapness

Momentum investing runs directly counter to the “buy low” instinct most retail investors are trained on. The strategy: rank stocks by their price performance over the past 6–12 months, and buy the strongest performers, on the premise that stocks which have been going up tend to keep going up for a while longer before mean-reverting.

This sounds almost too simple, but the persistence of the momentum effect across markets and decades is one of the more robust findings in empirical finance. In the Indian context, momentum has shown particularly strong results in mid-cap and small-cap segments, where information diffuses more slowly and institutional coverage is thinner, giving price trends more room to run before the market fully prices in new information.

The risk with momentum is sharp, fast reversals — momentum strategies tend to get badly hurt during market regime shifts, like the sudden reversal from growth to value that markets periodically experience, or sharp corrections where yesterday’s winners become today’s biggest fallers. Momentum strategies need disciplined rebalancing and position sizing precisely because the strategy’s strength (riding trends) is also its core vulnerability (getting caught when trends break).

Value: buying cheap relative to fundamentals

Value investing needs less introduction — it’s the Warren Buffett, Benjamin Graham lineage most Indian investors already have some intuitive relationship with. The factor version simply systematizes it: rank stocks on metrics like P/E, P/B, or EV/EBITDA relative to their sector or their own history, and tilt toward the cheaper end.

Value has had a more complicated recent history globally than momentum or quality — a long stretch through the 2010s where growth stocks (particularly tech) dramatically outperformed value, leading many to question whether the factor was “dead.” In Indian markets, value has shown cyclicality tied closely to broader market regime: it tends to work well coming out of market corrections and during periods when earnings growth broadens across sectors rather than concentrating in a handful of expensive growth names, and it tends to underperform during narrow, momentum-driven bull runs concentrated in richly valued sectors.

The practical lesson for Indian investors: value works, but it’s the factor most prone to long stretches of underperformance that test conviction. It rewards patience more than any of the other factors.

Quality: the factor that smooths the ride

Quality investing tilts toward companies with high and stable return on equity, consistent earnings growth, low leverage, and strong balance sheets. Unlike momentum and value, which can be volatile and cyclical, quality tends to be the most defensively-oriented factor — quality stocks typically hold up better during market downturns because the underlying businesses are simply more resilient.

In the Indian market specifically, quality has been a particularly effective factor given the market’s structural characteristics: a meaningful chunk of listed companies carry high leverage, inconsistent governance, or earnings volatility, which means a well-constructed quality screen filters out a real amount of downside risk that a simple index exposure wouldn’t.

Combining factors: why multi-factor beats single-factor

The most important practical insight from factor research isn’t which single factor is “best” — it’s that combining factors, particularly ones with low or negative correlation to each other, produces more consistent results than betting on any one factor alone. Momentum and value, for instance, tend to work in different market regimes and are often negatively correlated in their return patterns. A portfolio tilted toward stocks that score well on momentum, value, and quality simultaneously — sometimes called a “quality momentum” or multi-factor approach — has shown more consistent outperformance with lower drawdowns than single-factor strategies in Indian backtests.

How to actually access factor investing in India

You don’t need a Bloomberg terminal and a quant team to use this framework:

- Smart beta / factor ETFs and index funds now exist on Indian exchanges tracking momentum, value, quality, and low-volatility indices (e.g., Nifty200 Momentum 30, Nifty50 Value 20, Nifty Quality 30). These give you factor exposure with the cost structure and simplicity of an index fund.

- Factor-based mutual funds run by several AMCs now explicitly market themselves around a single or multi-factor strategy, with active management layered on top of the systematic screen.

- DIY screening using stock screeners is viable for investors who want to build their own factor tilts — ranking stocks on the relevant metrics and constructing a basket, rebalanced periodically (quarterly is common for momentum; annually is more typical for value and quality given their slower-moving nature).

What factor investing won’t do for you

It’s worth being honest about limitations. Factor investing is not a guarantee of outperformance in any given year — factors go through extended periods of underperformance, sometimes multiple years, and abandoning a factor strategy after a bad stretch (right before it recovers) is the single most common way investors destroy the actual long-term edge these strategies offer. Factor investing also isn’t free of risk simply because it’s systematic — a quality factor portfolio can still be concentrated in a handful of sectors, and a momentum portfolio can still get whipsawed in choppy, directionless markets.

The takeaway

Factor investing gives you a research-backed, testable framework for what “good stock picking” actually looks like when you strip away narrative and intuition. Momentum captures the market’s tendency to underreact to trends, value captures periods of mispricing relative to fundamentals, and quality captures the market’s tendency to occasionally undervalue balance sheet strength and earnings consistency. None of them work every year. Used together, with realistic expectations about patience and drawdowns, they’ve offered a durable edge over simple market-cap-weighted investing — one increasingly accessible to Indian retail investors through low-cost factor funds rather than requiring institutional infrastructure.