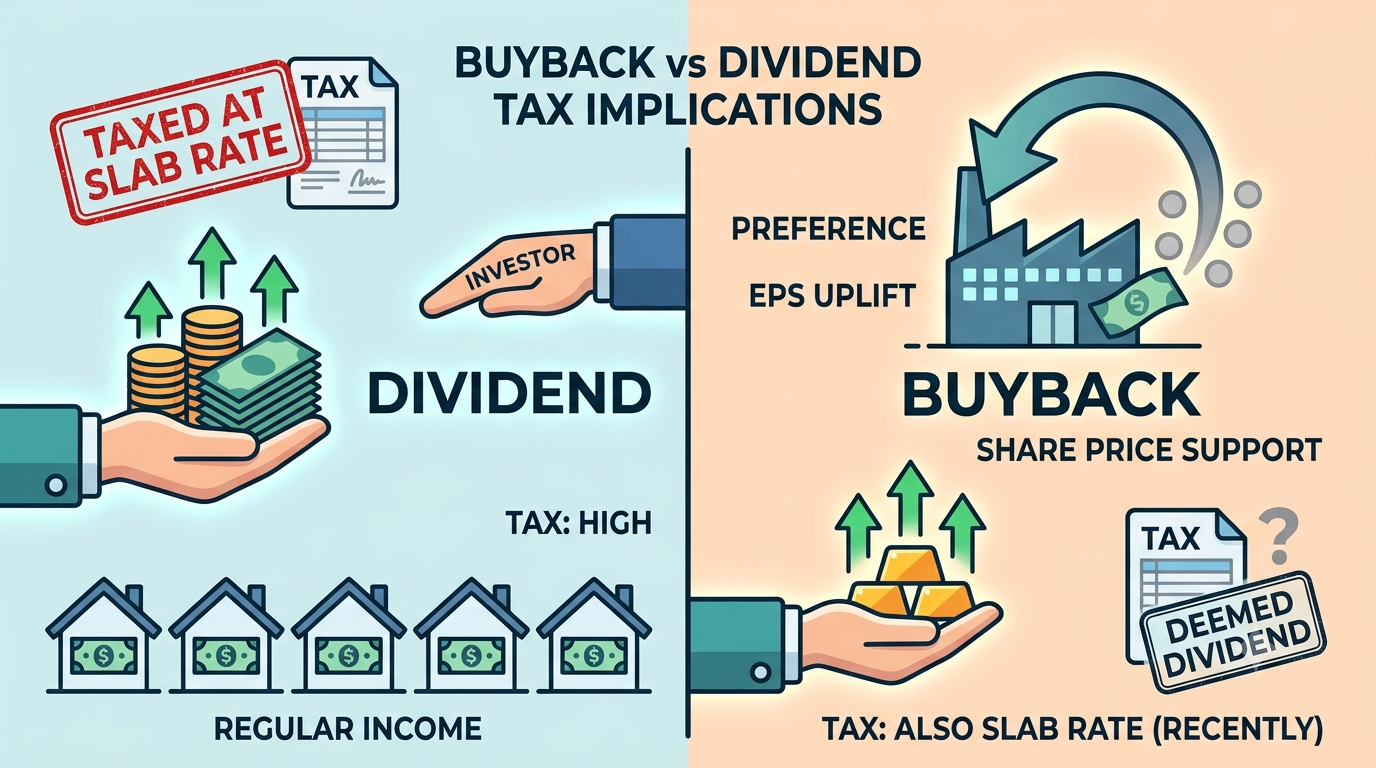

Buyback vs Dividend: Tax Implications Every Investor Should Know

When a company has surplus cash, it generally has two ways to hand some of it back to shareholders: pay a dividend, or buy back its own shares. Both look similar on the surface — cash moving from company to shareholder — but the tax and market impact are meaningfully different.

How dividends are taxed

Dividends are added to your total income and taxed at your applicable slab rate. If you’re in the highest tax bracket, that can mean a fairly significant chunk of the dividend disappearing to tax in the same year you receive it. Companies also deduct TDS on dividend payouts above a certain threshold, which you then reconcile at the time of filing your return.

How buybacks are taxed

For a while, buybacks were taxed differently at the company level under a separate buyback tax, making them attractive relative to dividends for many investors. That framework has shifted — buyback proceeds are now generally taxed in the hands of the shareholder, treated as deemed dividend income, taxed at slab rate, similar to how dividend income is handled. This has narrowed the tax-efficiency gap that buybacks used to offer, so it’s worth checking the current framework at the time you’re actually evaluating a specific buyback, since these rules have moved more than once in recent years.

Why companies still prefer buybacks in many cases

Even with the tax treatment converging, companies often still prefer buybacks because they reduce the total number of outstanding shares, which mechanically improves earnings per share and can support the stock price. It’s also a more flexible tool — a company can choose to do a buyback once without setting an expectation of doing it again, unlike a dividend, which shareholders tend to expect to continue.

What this means for you as an investor

If you’re holding shares in a company doing a buyback, you generally have the choice to tender your shares or hold on. Tendering converts your holding into cash (subject to whatever the current tax treatment is), while holding on means your proportional ownership in the company effectively increases as the total share count shrinks. Which is better depends on your view of the company’s long-term prospects, your own tax situation, and your reason for holding the stock in the first place — there’s no universally correct answer.