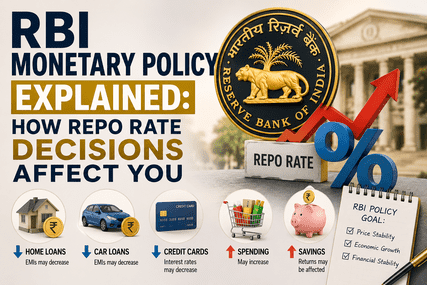

Every two months, six people sitting in a room in Mumbai make a decision that ripples through your home loan EMI, your fixed deposit returns, and the value of your equity portfolio. That’s the Monetary Policy Committee (MPC), and the decision is the repo rate. As of the June 2026 policy the 61st MPC meeting under Governor Sanjay Malhotra — the repo rate stands at 5.25%, held steady for a second consecutive meeting with a neutral stance, alongside a Standing Deposit Facility (SDF) rate of 5.00% and a Marginal Standing Facility (MSF)/Bank Rate of 5.50%. Understanding what’s behind a number like that, and why it moves or doesn’t, is one of the most useful pieces of financial literacy you can build.

What the repo rate actually is

The repo rate is the interest rate at which the RBI lends short-term funds to commercial banks against government securities as collateral. When banks need liquidity, they borrow from the RBI at this rate; when the RBI wants to absorb excess liquidity from the system, it uses the SDF, which now functions as the primary tool for that side of the corridor. Together with the MSF the ceiling rate banks pay for emergency overnight borrowing these form what’s called the “policy corridor,” the band within which short-term interest rates in the economy are meant to move.

Why the MPC exists and how it decides

The Monetary Policy Committee was created to take rate-setting out of the hands of a single individual and make it a collective, data-driven decision. Its primary mandate under India’s inflation-targeting framework is to keep CPI inflation within a 2–6% band, with 4% as the medium-term target. Every decision weighs that inflation mandate against growth considerations, because raising rates to control inflation slows borrowing and spending, while cutting rates to boost growth risks reigniting price pressures.

The June 2026 decision is a good real-world illustration of this balancing act. The committee revised India’s FY27 GDP growth forecast down to 6.6%, from 6.9% projected at the April meeting a meaningful downgrade driven largely by the West Asia conflict pushing crude oil prices up toward $110 a barrel for the Indian crude basket. At the same time, the CPI inflation projection for FY27 was revised upward to 5.1% from 4.6%, with food and energy costs doing most of that work while core inflation held relatively steady around 3.7%.

Faced with slowing growth and rising inflation simultaneously a genuinely uncomfortable combination for any central bank the MPC chose to hold rates rather than cut or hike. The logic: this inflation is imported, driven by external oil shocks rather than domestic demand overheating. Cutting rates wouldn’t fix the oil price; it would just add fuel-on-fuel demand pressure on top of already-rising costs. Hiking rates wouldn’t bring oil prices down either; it would just make borrowing more expensive for businesses and consumers without addressing the source of the problem. So the RBI holds, and watches.

How a repo rate decision actually reaches your wallet

This is the part most people skip past, but it’s the practical core of why this matters:

Home loans and floating-rate borrowing. Most retail loans in India today are linked to External Benchmark Lending Rates (EBLR), which are tied directly to the repo rate. When the repo rate holds, EMIs on these loans stay flat. When it moves, EBLR-linked loans adjust relatively quickly — often within a quarter — while older MCLR-linked loans adjust more slowly, since MCLR resets are staggered and incorporate the bank’s own cost of funds.

Fixed deposits. Banks tend to adjust FD rates in the same direction as the repo rate, though not always by the same magnitude or on the same timeline. A rate hold, as in the current cycle, generally means FD rates stay in a stable band which is part of why several banks have been encouraging depositors to lock in current rates for 1–3 year tenures rather than staying in short-duration instruments.

Equity markets. Lower rates generally support equity valuations by making future earnings worth more in present-value terms and by reducing the relative appeal of fixed income. A prolonged hold, especially one accompanied by a lowered growth forecast, tends to create a more mixed market reaction — rate-sensitive sectors like banking, auto, and real estate benefit from the removal of uncertainty even without a cut, since predictable borrowing costs support planning and demand.

Bond markets. A steady repo rate combined with a neutral stance typically stabilizes bond yields, which matters directly if you hold debt mutual funds, government securities, or any fixed-income product where returns are sensitive to yield movements.

Reading the stance, not just the number

One nuance worth understanding: the RBI’s “stance” (accommodative, neutral, or withdrawal of accommodation) often tells you more about future direction than the rate itself. A neutral stance, which is where the MPC currently sits, signals the committee is data-dependent and not committed to a particular direction — it will cut, hold, or hike based on incoming data, with no bias baked in. That’s different from an accommodative stance, which signals a bias toward supporting growth even at the cost of somewhat higher inflation.

What to watch heading into the next decision

The next MPC meeting is scheduled for August 4–6, 2026, and a few variables will likely determine the outcome:

- The trajectory of the West Asia conflict. A ceasefire and normalized oil flows through the Strait of Hormuz would ease the single biggest inflation risk currently on the RBI’s radar and could open the door to a resumed rate-cutting cycle later in the year.

- The June and July CPI prints, particularly whether core inflation (which strips out food and energy) stays contained even as headline inflation runs hot.

- Monsoon progress relative to IMD forecasts a weak monsoon adds food inflation on top of energy-driven inflation, tightening the RBI’s room to maneuver further.

The takeaway

The repo rate isn’t an abstract number for economists — it’s the mechanism through which the cost of money in the entire economy gets set, and it flows through to nearly every financial decision you make, from the EMI on your home loan to the yield on your fixed deposit to the multiple the market is willing to pay for stocks. Understanding not just where the rate sits, but why the MPC chose to hold, cut, or hike, gives you a genuine edge in reading where borrowing costs, deposit returns, and market sentiment are headed next.