If you’ve tracked quarterly results over the past few years, you’ve probably noticed a pattern: more companies are announcing share buybacks, and fewer are sweetening dividends the way they used to. This isn’t a coincidence or a passing trend. It reflects a real shift in how boards think about returning cash to shareholders, and understanding why can make you a sharper reader of company announcements.

What a buyback actually does

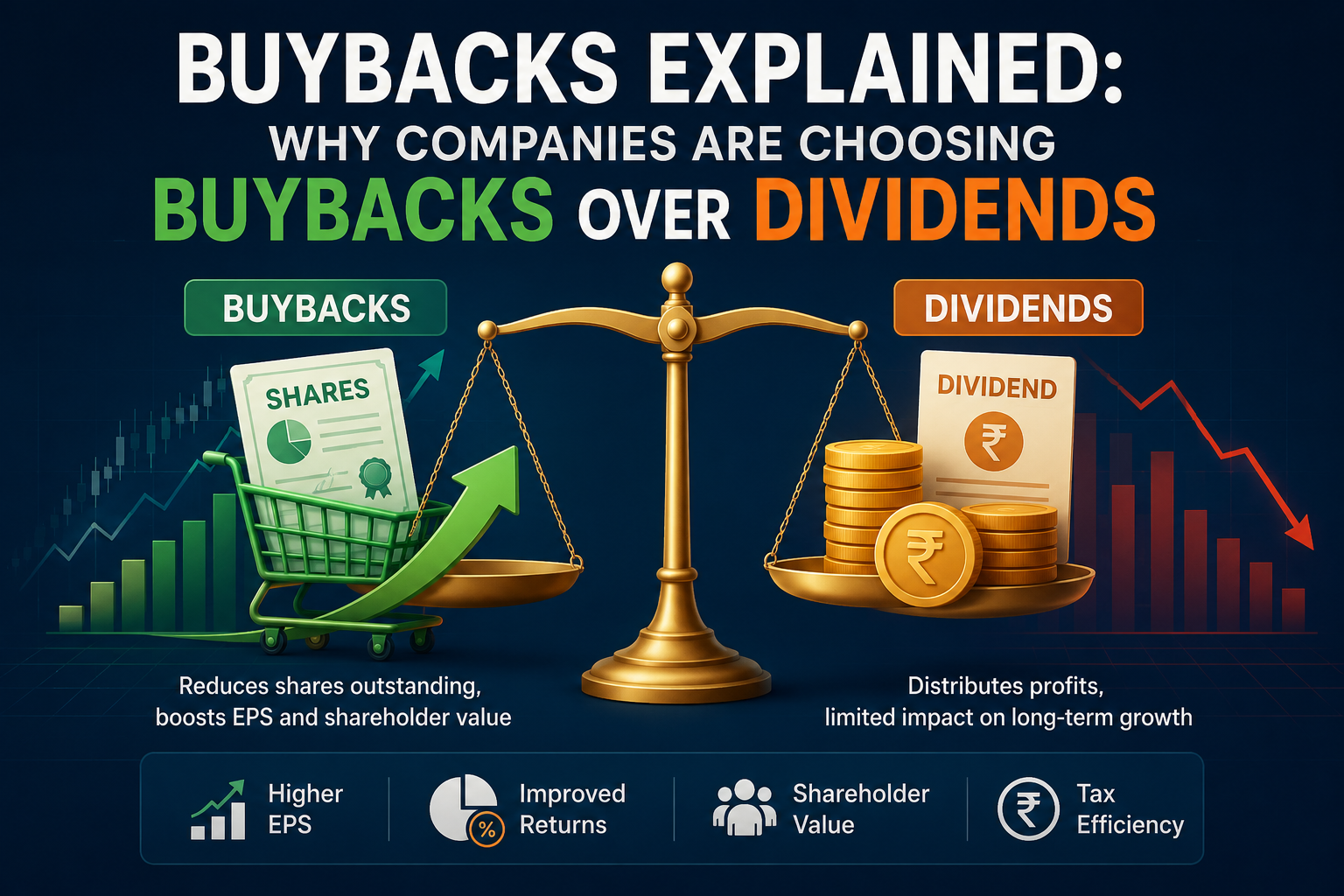

A buyback (or share repurchase) is when a company uses its own cash to purchase its shares from the open market or through a tender offer, then extinguishes them. The share count shrinks, which means each remaining share represents a slightly larger slice of the company. Earnings per share go up mechanically, even if the underlying profit hasn’t changed at all.

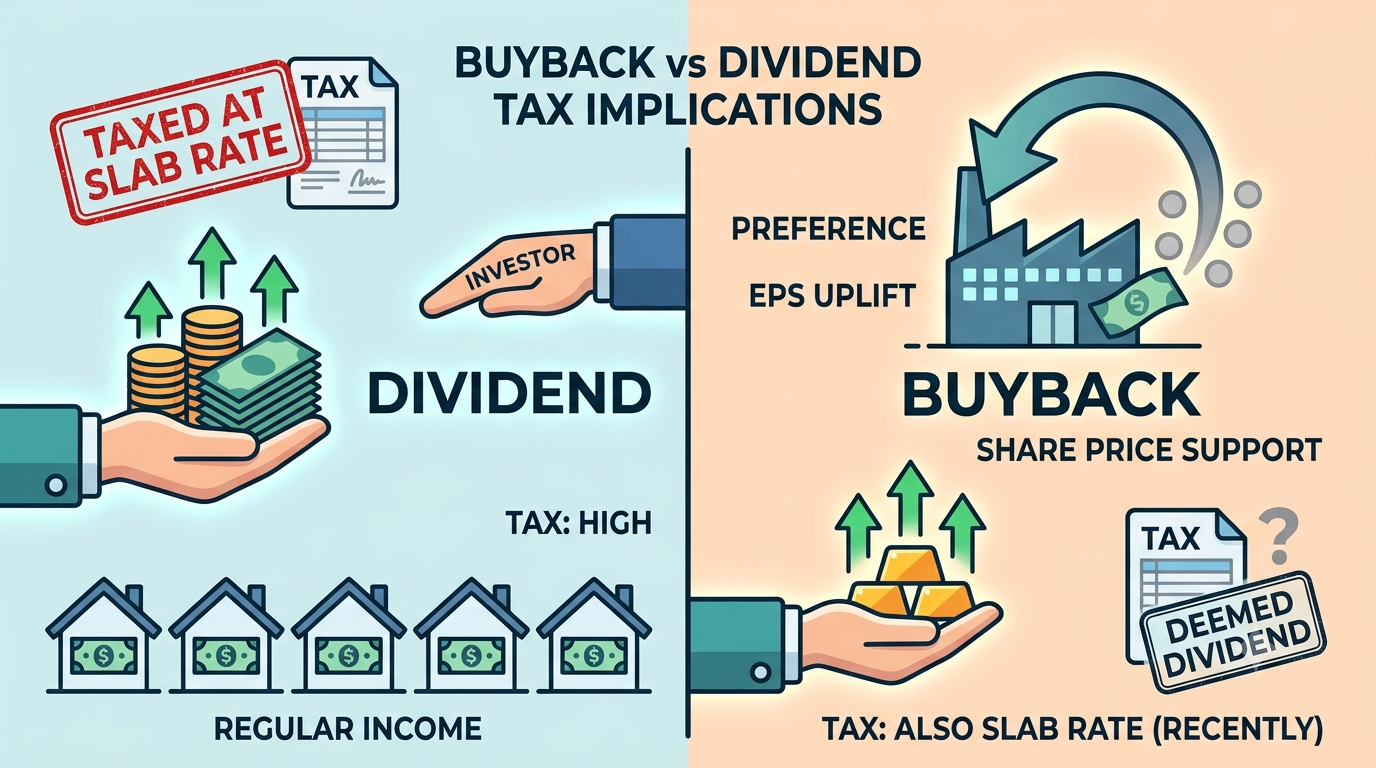

A dividend, by contrast, is a direct cash payout to shareholders, taxed as income in most jurisdictions and locked in as an expectation — cut a dividend and the market usually punishes the stock hard.

That difference in market psychology is the first reason buybacks have become the preferred tool.

The flexibility argument

Dividends create a commitment. Once a company starts paying a steady dividend, investors expect it to continue or grow, and any reduction is read as a signal of distress. Buybacks carry no such promise. A company can run a buyback this year and skip it entirely next year without anyone assuming the business is in trouble. For management teams navigating unpredictable earnings — which, in a post-pandemic, rate-volatile environment, describes most of them — that flexibility is valuable.

The tax angle

In many markets, including India, buybacks have historically carried a different tax treatment than dividends, and this has shaped corporate decisions considerably. Buyback proceeds were, for a period, taxed at the company level rather than as dividend income in the shareholder’s hands, which made them more attractive to promoters and large shareholders who fall into higher tax brackets. Even where rules have converged over time, the way gains are classified — as capital gains rather than dividend income — often still works out more favourably for long-term holders. This is one of the quieter but more powerful reasons buybacks have gained ground: they are frequently just a more tax-efficient way to move cash from the company’s balance sheet to the shareholder’s pocket.

Signalling undervaluation

When a company buys back its own stock, it is implicitly telling the market: “we believe our shares are worth more than the current price.” Whether or not that’s true, the signal itself often moves the stock. Promoters and management, who typically have the best information about the business, choosing to deploy cash into their own shares rather than expansion, acquisitions, or debt repayment is read as a vote of confidence. This is particularly potent for IT services and pharma companies in India, where large cash piles sitting idle have historically drawn criticism from shareholders demanding capital be put to use.

What buybacks say about a company’s growth stage

There’s a less flattering read on this trend too. Companies buy back stock instead of investing in growth when they’ve run out of high-return projects to fund internally. A mature, cash-generative business with limited reinvestment opportunities is a textbook buyback candidate. If you see a company shift from heavy capex and reinvestment toward consistent buybacks, it can mean the business has entered a slower-growth phase — not necessarily bad, but worth noting as you assess the stock’s future trajectory.

What to actually check before reacting to a buyback announcement

A buyback headline alone tells you very little. Before treating it as a bullish signal, look at:

- The size relative to market cap. A buyback covering 1% of outstanding shares is largely cosmetic; one covering 5–10% is meaningful.

- The price band versus current market price. If a company is buying back shares well above where they’re trading, that’s a stronger signal of confidence — and a real transfer of value to remaining shareholders — than a buyback priced near the market.

- The funding source. Buybacks funded from free cash flow are healthier than those funded by fresh debt, which simply re-leverages the balance sheet to boost EPS optically.

- Promoter participation. Under Indian buyback rules, promoters can choose whether to tender their shares. If promoters are not participating and are instead letting their stake rise as a percentage of a shrinking float, that’s often the real intent behind the exercise.

The bigger picture

The shift toward buybacks isn’t unique to India — it mirrors a global trend, most visible in the US market over the last two decades. But the drivers in India have their own local flavour: promoter tax efficiency, large IT and pharma companies sitting on cash reserves built during high-growth years, and a regulatory framework under SEBI that has made the buyback process faster and more standardised than it once was.

For investors, the practical takeaway is this: don’t treat a buyback announcement as an automatic buy signal. Treat it as a data point that tells you something about management’s view of valuation, the company’s growth stage, and its capital allocation discipline — and then check that data point against the size, pricing, and funding of the buyback itself before deciding what it’s really telling you.